The carbon market gained notoriety from the signing of the Kyoto Protocol in 1997 and its final implementation in 2005. The Protocol established that developed countries should have targets for reducing greenhouse gas (GHG) emissions and that developing countries' development could help developed countries achieve their goals more cost-effectively.

In a specific way, an arrangement was established for countries that until that time didn't have any mandatory emission reduction targets could develop projects generating Certified Emission Reductions (CERs). Now it could be negotiated with countries that had reduction targets defined by the Protocol. The arrangement for collaboration between developing and developed countries so that the latter meet the established reduction targets was called the Clean Development Mechanism (CDM), whose targets should be achieved within a period ending in 2021. Through this mechanism, an international market for carbon credits was created, where the demand for credits came from countries obliged by the agreement to meet their targets, and the offer came from host countries of GHG emission reduction projects.

Despite being considered the main milestone in the creation of the regulated market for carbon credits, the market created from the Kyoto Protocol had restrictions related to the types of methodologies implemented for the development of projects and the sectoral scopes of action, which caused the exclusion of some participants and projects that did not meet the CDM rules.

Thus, in parallel with the Kyoto Protocol carbon credits market, initiatives emerged in the international market not linked to this agreement, called the Voluntary Carbon Market. In this environment, with specific rules and methodologies, companies and institutions that did not have legal obligations to reduce emissions, but wished to offset them, could acquire carbon credits in this new market.

The high transaction and project development costs in the CDM made it impossible for many companies to participate as project proponents. The voluntary market emerged with the proposal to open space for the initial development of projects on a scale that would not be economically viable in the market regulated by the KP. In this sense, by establishing the guidelines that allowed the shaping of the credit trading infrastructure in the regulated field through the CDM, the KP also indirectly contributed to the determination of the first standards for carbon offset methodologies in the voluntary field.

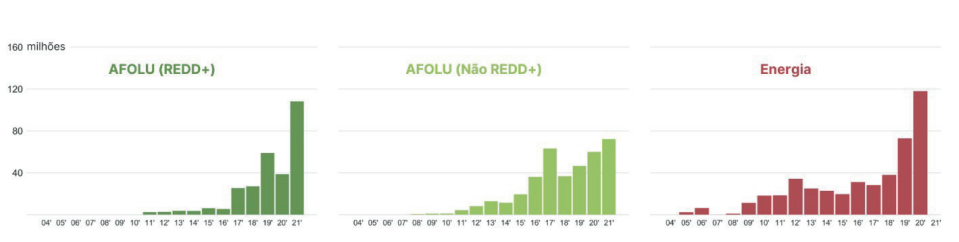

As a result of the growing recognition of the importance of reducing GHG emissions, many companies and individuals are looking to reduce their carbon footprints. Motivated by socio-environmental responsibility and the possibility of enhancing the institutional image in terms of sustainability, these organizations are increasingly resorting to offsets generated in the voluntary carbon market to achieve emission neutrality. Below we can see the global evolution of carbon credits generated in the voluntary market between 2002 and 2021.

The graph above shows that the growth of the voluntary carbon market intensified from 2015 onwards, with greater emphasis from 2019 onwards. According to the World Bank (2021), the increase in carbon credits emissions is mainly due to the increasing demand from companies on all continents that have adopted commitments to reduce their net GHG emissions to zero.

Besides, we can observe that the sectors who have stood out in the Credits Generation in the voluntary global market in recent years are the production or conservation of energy and forest (REDD+1 and not REDD+). Regarding credits generated through energy projects, it is noted that emissions from these credits increased approximately 2.5 times between 2019 and 2021. Regarding credits generated by forestry projects based on REDD+ actions, emissions were almost quadrupled in the last four years.

According to the World Bank, the significant increase in the carbon credits emissions from energy production or conservation projects can be explained by two main reasons. The first reason is related to the fact that these credits are among the ones with the lowest generation cost. Consequently, it's the type of credit with the lowest price among those available on the market. The second reason is that the main international standards for certification of carbon credits no longer allow the registration of renewable energy projects in some locations as of 2020.

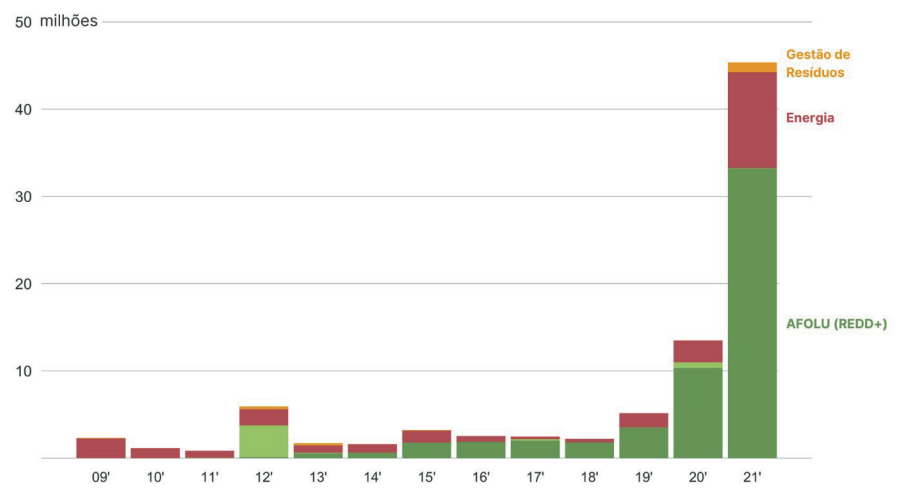

On the national scene, the growth in emissions of carbon credits over the last few years is even more expressive.

The graph above shows that the volume of credits generated in 2021 was increased by 236% compared to the volume generated in 2020 and by 779% compared to the volume generated in 2019. As in the international voluntary carbon market, this increase may have been driven by the high demand on the part of the business sector to meet the assumed neutrality commitments.

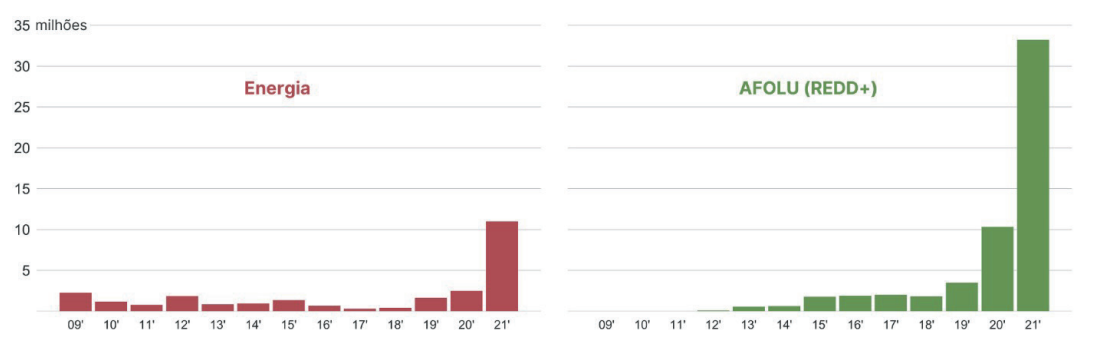

Following the international market trend, the significant increase in the number of credits generated was led by the energy production and conservation sectors and by the REDD+ type forestry sector projects, as can be seen in the chart below. In the last two years, the amounts of credits issued by energy and REDD+ projects have increased by more than 5 and 8 times, respectively.

The justifications for the robust increases in credit issuance shown by the above graph are likely to be the same as for the increases seen in the international voluntary market. In the case of credits generated by energy projects, the justification lies in the expectation that interest in them will decrease in the future. Concerning the credits generated by forest projects of the REDD+ type, the justification is due to the high demand for solutions based on nature.

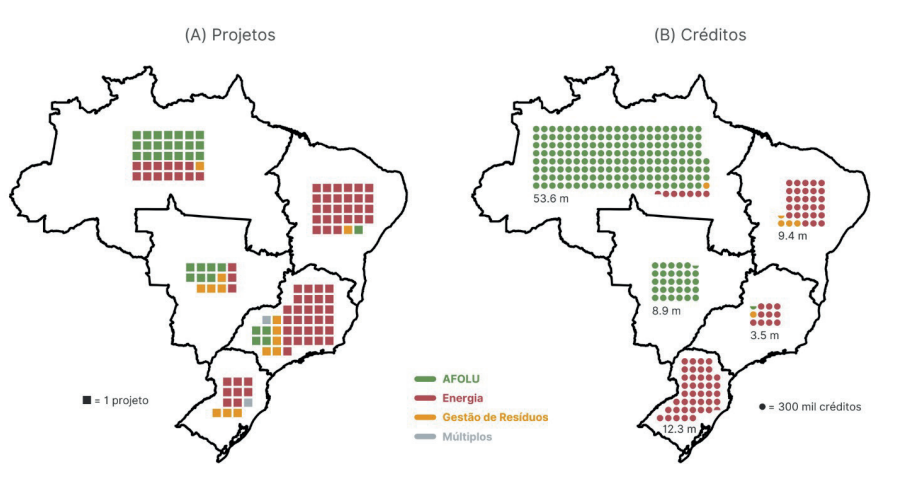

Brazil has a prominent position on carbon credits generation in the voluntary global market. Currently, the country holds the fourth position in carbon credits volume historically generated in this type of market, behind only the United States, India, and China. Despite its expressiveness in the already generated credits volume, the country is less prominent in projects that generate credits. While the leaders of the United States and India individually have more than a thousand projects registered or under development/validation, Brazil ranks eighth, with only 159 projects, behind countries like Rwanda, Uganda, and Kenya.

The Brazilian market currently has 159 projects, including projects already registered by the certification standards and projects under development or validation. Of those projects, 80% are registered projects that have already generated credits since their registration, 4% are registered projects that have not yet had certified credit emissions, and 15% are under development or validation. Among these registered projects, 89% are VCS certified projects, 7% are GS certified, and 4% are ACR certified.

Following the international trend of increasing project registrations, 6% of the total registered projects had emissions of credits certified for the first time in 2020 and 5% in 2021. The projects that had their first emissions certified in 2020 corresponded to 15% of the total generated credits that year, while this amount was 18% of the total credits generated in 2021.

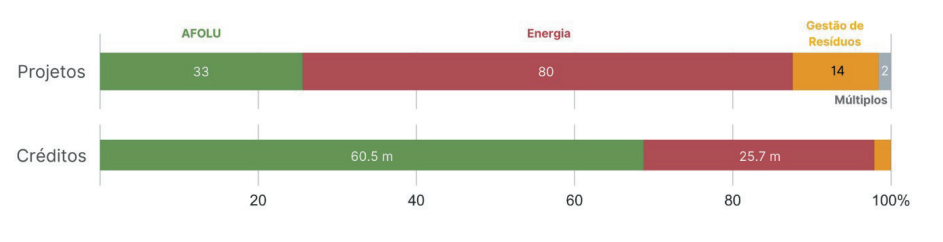

The Brazilian market is mainly dominated by Energy projects (63%), followed by Agriculture, Forestry, and Other Land Use (AFOLU) projects (25%). However, despite the number of energy projects, it is observed that the volume of credits generated by projects related to the AFOLU sector is significantly higher. In 2020 and 2021, the share of credits generated by these projects was 81% and 73%, respectively, while credits generated by energy projects had a share of 18% and 24% in those same years.

About 26% of the registered projects are located in the North region. 29% gets in the Southeast region, and 44% in other parts of the country. The North region generated 61% of the total credit history, which, compared to the volume of projects registered in the region, demonstrates the expressiveness of these projects in terms of their ability to generate offsets for GHG emissions.

The regional analysis of the scope of activity of the registered projects shows that almost all the credits generated in the Midwest and North regions come from AFOLU projects (99% and 96%, respectively). The generated credits in other regions are predominantly from energy generation and conservation projects, especially in the South region, where practically all credits are generated by projects with this scope of activity.

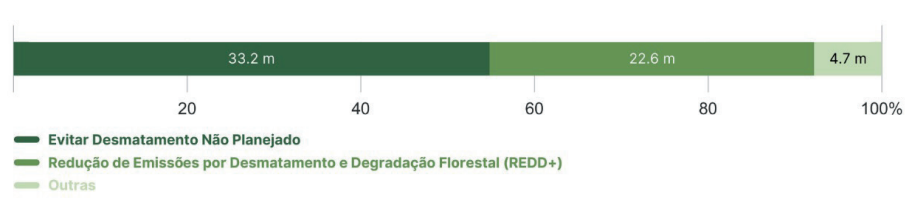

The analysis of the methodologies used in the registered projects shows that among the compensations coming from AFOLU Projects, 55% come from projects that use those methodologies to avoid unplanned deforestation. In resume, this methodology estimates GHG emissions from areas where unplanned deforestation occurs and quantifies the emission reductions achieved by containing deforestation.

Another methodology that represents the credit generation from AFOLU projects is the methodological structure of REDD+, which corresponded to 37% of the total credits generated by this scope of activity. This methodology quantifies GHG emission reductions by avoiding planned and unplanned deforestation and forest degradation, in addition to quantifying offsets resulting from afforestation, reforestation, and revegetation activities.

It is worth mentioning that, despite the representativeness of the projects in the AFOLU sector in the total carbon credits generated in Brazil, the projects are mostly related to the forestry sector. The number of projects in the agricultural sector registered so far, as well as the volume of credits generated by them is not very representative and is limited to the methodology of methane recovery through the treatment of livestock waste.

Regarding the methodologies used in the Energy Projects, 61% of generated credits came from electricity generation projects connected to the grid of renewable sources. This methodology consists of rehabilitation (or retrofitting), replacing or adding capacity to an existing plant, or building and operating a new plant, which uses renewable energy sources and supplies electricity to the grid. Another representative methodology in the total of credits historically generated in the energy sector is the one referring to the exchange of non-renewable biomass for renewable biomass for the generation of thermal energy. This methodology was responsible for 19% of the credits historically generated by projects in this sector.

Of the total generated credits using the electricity generation methodology connected to the grid from renewable sources (from 2009 to 2021), 57% came in 2021. The significant issuance of offsets using this methodology in that year is probably due to the expectation that in a short time, the credits generated by these projects will no longer be additional and, therefore, will cease to generate income.

It is expected that the credit generation by projects with this scope of activity will occur very intensively once they still are considered as additional. It will be driven by the high demand for those credits due to their lower price compared to the generated credits for the projects with other scopes.

The process of generating and trading credits in the voluntary carbon market consists of 4 main stages, in which different agents play very important roles throughout the process.

The elaboration of a project that generates carbon credits starts by identifying the potential activity to reduce or remove GHG emissions and verifying its feasibility. The activity identification goes hand in hand with the methodology chosen for the project implementation.

The methodology defines the detailed procedures for quantifying the reductions/removals of GHG emissions that may generate carbon credits. It establishes the criteria and conditions for determining additionality and the crediting baseline for given the scope project. International certification standards recognize a set of pre-approved methodologies within the scope of the International Regulated Market or by a specific scientific group.

If any methodology can apply to the specific project, it is also possible to propose the development of a new methodology. In that case, the developer must submit the new methodology to an independent validation procedure. The proposed methodology will first be known as a Designated Operational Ent (DOE). The DOE assessment report will then be reviewed, and if it meets the independent mechanism's reliability standards, the approval will finally be approved.

The current methodologies were designed by developers from different parts of the world. Among them, two methodologies designed by Brazilian developers stand out.

The first one is the Methodology for Avoided Unplanned Deforestation, which was developed by the Sustainable Amazon Foundation (FAS) in partnership with the BioCarbon Fund, Carbon Decisions International, and the Institute for Conservation and Sustainable Development of Amazonas (Idesam). This methodology is used for monitoring GHG emissions from project activities that prevent unplanned deforestation. In addition, it also allows accounting for increases in carbon stock in forests that would be deforested in the baseline scenario.

The second Brazilian methodology is the exchange of gasoline for ethanol in fleets of flex-fuel vehicles, developed by Keyassociados and Ecofrotas and approved in 2012. This methodology calculates the reductions in GHG emissions resulting from gasoline for ethanol replacement or by blending ethanol with gasoline (with at least 95% ethanol) in commercial fleets of flex-fuel vehicles. Since its approval, this methodology has already been used in two projects, one in Brazil and another one in India, generating approximately 43,000 carbon credits.

Given the requirements for credit-generating project implementation, potential bidders often need to turn to specialized companies for its development. These company's activities in the project elaboration include the definition of the methodology to be used and the mapping of the potential activity to generate compensation as a demonstration that the project meets the requirements demanded by the certification standard. Given the requirements for credit-generating project implementation, potential bidders often need to turn to specialized companies for its development.

These company's activities in the project elaboration include the definition of the methodology to be used and the mapping of the potential activity to generate compensation as a demonstration that the project meets the requirements demanded by the certification standards.

The quality requirements that fall on projects must ensure that emission reductions or removals are:

- Real and measurable;

- Additional, that is, they must guarantee that emissions would not occur without the revenue from the sale of carbon credits generated;

- Permanent, which means that projects must ensure that reductions or removals weren't lost due to unforeseen events (such as GHG removals lost due to fires);

- To be unique: the credits emissions are numbered exclusively to guarantee that there is no double counting of GHG reductions.

The developed projects are categorized into sectoral scopes and include a variety of technologies and ways of measuring GHG reductions or removals. These are some of the scopes that each project can be developed: energy (renewable and non-renewable), energy distribution, energy demand, manufacturing industries, chemical industries, construction, transportation, mining/mineral production, metals production, emissions fugitive fuels, fugitive industrial gas emissions, solvent use, waste handling and disposal, forestry and reforestation, and agriculture.

After its development, the project needs to be validated and monitored by the DOEs, independent audits accredited by the certification standards. The central role of these audits is to ensure the project's faithful observance of the required standards and applied methodologies. Different DOEs were responsible for validating Brazilian projects, and 8 DOEs perform the validation of 80% of these projects. It is worth noting that among the active DOEs approved by the certification standards, none are Brazilian.

The only national audit approved by the Standards is the Brazilian Institute of Public Opinion and Statistics (IBOPE), which has been inactive since 2015. Despite this, some national institutions were accredited by DOEs approved by the certification standards to carry out the project's audition. This is the case of Imaflora (Instituto de Manejo e Certificação Florestal e Agrícola), an NGO accredited by the Rainforest Alliance for the validation of forest projects, and Verifit, representative of Earthood Services.

At the end of the validation process, the proponents request for their projects to be registered in the certification standards, therefore, being able to issue carbon credits in the voluntary market. After the project becomes operational, its proponents must carry out project monitoring, which consists of tracking and reporting GHG emission reductions.

Reductions accounted for in monitoring must also be verified and validated by DOEs. The credits generated by the projects need to be certified to guarantee that they are intact and that they are equivalent to a reduction of one unit of tCO2e.

After registration and certification, carbon credits are generated by the certification standard to which the developed project is linked. Credits are released in batches according to the expected volume to be issued yearly in the project's absence. Offsets can be purchased and withdrawn by end users to offset their emissions, that can be either companies or individuals. The carbon credits purchase can be negotiated with the companies that develop the projects, which also sell the credits generated by it.

Companies who wish to purchase emission offsets must, together with project developers, prepare an emissions inventory to measure their direct and indirect emissions. The inventory then establishes the volume of credits that must be acquired to reach the interested company's emissions neutrality.

Some developers have their online platforms, such as the Green Forest Carbon platform, where it is possible to calculate the individual carbon footprint and purchase credits to offset GHG emissions.

The platform's calculators use questions such as average electricity, gas, and water consumption, annual mileage in owned vehicles, average time spent on public transport, and air travel amount to estimate the total carbon emitted per person. After that, it estimates how many carbon credits need to be purchased to offset the emissions made over a year.

In some cases, the platform allows choosing the project where the credits that will be acquired were generated. A survey carried out in December 2021 found that the value of the carbon credit available for sale to individuals on national platforms varies between R$60 and R$110. Although each credit represents a ton of carbon dioxide equivalent, the prices of credits may vary. Among the factors that result in price variation, can be cited the value associated with the additional benefit resulting from the credit-generating project, the costs necessary to develop, implement and monitor the project and the dynamics of supply and demand for credits from projects of different sectoral scopes.